Our brains are terrible at exponential growth.

A 1% fee sounds tiny. The difference between 0.25% and 1% is only 0.75% — who cares, right?

But here’s what our brains can’t see: that tiny percentage compounds year after year, quietly siphoning off your returns. Over a 40-year career, it adds up to a six-figure difference.

The maths that should make you uncomfortable

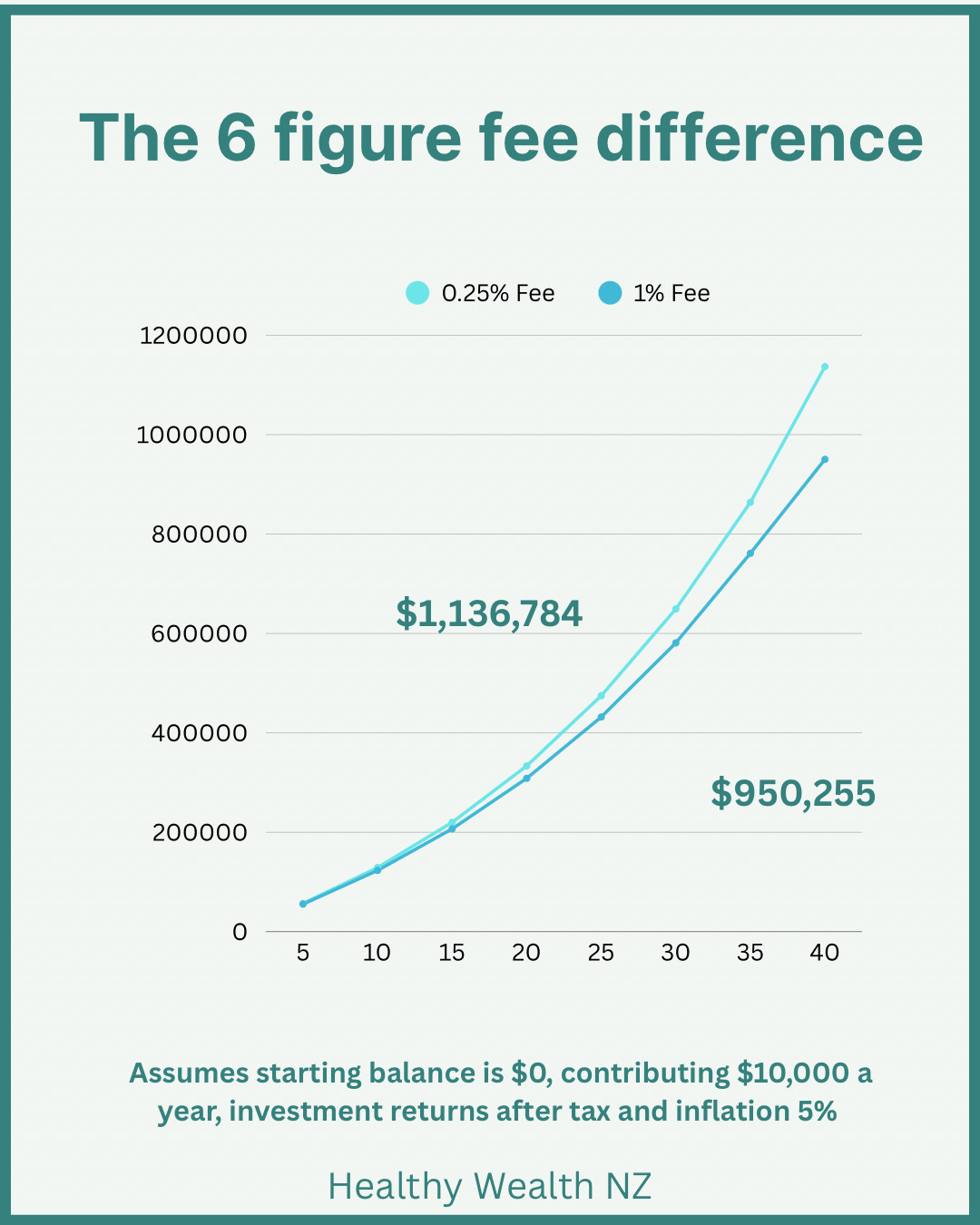

Let’s say you contribute $10,000 a year for 40 years, with a 5% return after tax and inflation.

At 0.25% fees, you end up with $1,136,784.

At 1% fees, you end up with $950,255.

That’s a $186,529 difference. Not because of bad investments. Not because of market crashes. Just fees.

And the higher your returns or contributions, the more pronounced the difference becomes. Fees don’t just take a cut — they take a cut of your compounding. It’s a leak that gets bigger over time.

A medical analogy

Think of fees like plaque building up in your arteries.

You don’t feel it happening. There’s no pain, no symptoms, no alarm bells. Year after year, everything seems fine. Your investments are ticking along, your balance is growing, and you assume you’re on track.

Then you hit retirement, ready to enjoy the fruits of 40 years of investing — and you discover your portfolio has been quietly narrowing the whole time. That six-figure difference? It’s not dramatic. It’s not a heart attack. It’s just… less capacity than you thought you had.

The cruel part is you’ll never see the money you lost. There’s no statement showing “here’s what you’d have if fees were lower.” You only see what you ended up with — and assume that’s how it was always going to be.

So are high-fee funds always bad?

No — but you need to know what you’re paying for.

Some funds charge higher fees because the active management involves additional screening for ethical investments, or they’re doing genuine impact work. That might be worth it to you.

The problem is when you’re paying high fees for nothing special. Many doctors are sitting in default KiwiSaver funds charging around 1% without realising — and those funds often aren’t doing anything that justifies the cost.

How to check your fees

Under 0.5% is generally considered low. Over 1% and you should be asking serious questions about what you’re getting.

You can find your KiwiSaver fees on your provider’s website or your annual statement — look for the “total fund charge” or “management fee.”

And if you’ve never checked? You’re probably not alone. But now you know why it matters.

This post is for educational purposes only and is not personalised financial advice.